In recent years, the tech landscape has been abuzz with the promise and potential of an Artificial Intelligence (AI) technology advancement which would allow to relaunch the market. It has been been a long wait, but here we are. Most companies rush to integrate AI technologies into their products, with every company trying to put the word AI in its guidance report in the hope to see its market capitalization grow since investors are eagerly seeking to capitalize on this burgeoning market. The subject of quantifying this future marketsize is still an ongoing debate as nobody is able to truly understand the demand and the future AI application impact on products and services. One of the most prominent players in this arena is Nvidia, whose stock price has soared on the back of its AI-related ventures. However, as excitement around AI stocks reaches fever pitch, some analysts are sounding the alarm, warning that these valuations may be indicative of a speculative bubble.

It is important to remind everyone that the psychological mindset of the market is quite polarized by the fact that we are facing a truly fascinating period, and that tech is starting to be a subject moving too fast for our common mind. As it is not an overstatement to assume that most people are optimistic on the AI subject, it should be interesting to remind everyone that the covid crisis exerted adverse impact on major equity markets. What I call the global investor, meaning the market, was praying for a recovery.

What he didn’t expect, was that he wouldn’t get a classic recovery, but an absolute AI boom. If I summarize, we were in a dark period in which every equity investor was suicidal when looking at his stock portfolio, and almost 2 years later, he’s facing a bull market like he has never seen in 20 years. There is no way that the common investor is staying rational in this situation. AI stocks were his savior, it is now his battle horse.

There is no way that his valuations (if he even do business valuation) are not disturbed by his overoptimism. The excitement surrounding AI stocks is understandable given the transformative potential of AI technologies, but these valuations may be unsustainable when you see how much people have jumped in the AI stock train. Everyone wants a piece, completly discarding the essence of valuation.

The valuations of many AI stocks, including Nvidia, have reached dizzying heights, far outstripping their underlying fundamentals. Price-to-earnings ratios and other traditional valuation metrics are often sky-high, raising concerns about overvaluation (you can see my valuation here). My personal valuation on the subject caused me issues on finance forums but since then we have seen a -15% decline, stating that I was not wrong on the subject. We are only at the beginning in my opinion. Future earnings reports will bring back reality in the minds of people and they will realize that the demand will be different to what they expect. In the long term, mayble the demande is what they expect, but the short term target is not what they think.

The hype surrounding AI stocks has led to a fear of missing out (FOMO) among investors, driving prices even higher. This herd mentality can fuel speculative bubbles, as investors pile into stocks without fully understanding the real demand and mechanisms.

It truly reminds me of the dot com bubble and you can’t deny me that right. I compare both situations in my NVIDIA stock analysis and as time goes by, the more I’m convinced that I’m right.

That is why I closed my entire position in MSFT, as I don’t want to partake in this madness as valuation as been too uncomfortable for my own taste, and I don’t want no shares in an object of speculation. Yes, even after buying MSFT at 240$/share and making a +77% gain (I sold at 425$), I still sold my winner. At the current moment, the only AI stock I still own is GOOGL that I bought sub 100$.

Only thing that you have as a value investor, is your investment principles, and even when it feels unnatural, you have to follow them.

As you know, diversification has been massively promoted as the optimal way to reduce risks and allows you to extend the reach of potential returns on multiple stock investments, something that you wouldn’t be able to do if you own only a few stocks.

But obviously, diversification has the strong tendency to reduce the returns of your biggest winners, furthermore producing more than average results, since from my opinion you can only have a few winners in your portfolio, as really good opportunities are not as numerous as you would think. It can also be added that investors that focus on diversification, underestimate the energy that is required from them whenever rebalancing their portfolio is needed since you have to search for the right investment(s) (which is already a big responsibility in itself) to make sure that you respect “your diversification requirements”. Therefore, it can cause you to be forced to make a bad decision since you are limited in your investments choices as some of your greatest investments, if there are too big in weight, become automatically prohibited to respect the principle of diversification. The phenomenon can truly appear to be unnatural as you have to restrict yourself from enjoying a potential moat that could return you much more than could be fathomed.

Starting from these arguments, I should mention that the reasons behind why I am so particularly prone to have a concentrated portfolio is because my risk appetite, at that specific moment in my life, allows me to. As a concentrated portfolio is riskier but enables more returns, I strongly think that this strategy is the best for someone that is starting to invest and/or still has to grow his capital. For a lack of words, there is no better moment to take that many risks.

Reading the book Richer, Wiser, Happier: How the World’s Greatest Investors Win in Markets and Life from William Green, it came to my attention that some fund managers mentioned in book, such as Eveillard, never had the stomach to hold a concentrated portfolio to the contrary to individuals like Buffett and Munger. That fact made me realize that to own a concentrated portfolio you either must be absolutely certain in the quality of your investments, or exceptionally unaware. While some very talented investors such as Eveillard could not put their money in only a few securities as it would kill them of stress, other legendary investors admitted that you only have a few ideas, meaning that it is very difficult to find that many exceptional companies priced at fair or low price, admitting that to have that many investments thesis would be just impossible.

In my modest quality as a still young and learning value investor, I personally have witnessed that I am not able to find more than 5 to 10 qualitative investment thesis concerning stocks in sectors that I feel sufficiently comfortable, in which I absolutely trust the outcomes going my way.

To be able to put around 1/3 of your portfolio behind your idea might seem very stupid to most people, but if you are confident enough in your process, meaning that the facts behind your reasoning are so oblivious after long searches that there is so little room for mistakes, why would you not seize the opportunity?

And I am going to conclude by saying this: if it is too stressful for you to own a small list of stocks, then it means that you shouldn’t even invest in it.

First, I would like to say that I personally enjoy NVIDIA products on the basis that their GPUs are a product that I am familiar with, and it has been the case for probably more than a decade. Now, my experience with their products is quite simple: premium quality for a high price. Does the price reflect the true value of the product? My opinion would tend towards a no, even if I do enjoy their products and ability to innovate in the gaming atmosphere. Anyway, if I wanted a price/value GPU, I would prefer to look into AMD’s, but that’s only my two cents on the subject and from what I know, that simple statement could truly cause mayhem on Tech forums and has been a debating matter for quite some time.

Now that you know that I am not biased towards NVIDIA and that I look at the company with a critical eye, you can understand that I’ve watched it develop marketing strategies to push their new GPUs at colossal prices and justifying them by highlighting that the ray tracing performance, DLSS, and cost-energy ability are sound arguments that establish the price as worth it.

I do understand and respect their alignment, nonetheless past lessons concerning the company have taught me that they are accommodated with empty promises. When I say promises not respected, I particularly think about those last booming years concerning the demand of GPUs, and the fact that shareholders were convinced by press releases and communications that NVIDIA would capitalize on that demand to increase sales volume and adjust overall prices to be more accessible (and align more with the price to quality ratio).

You are probably asking yourself, if this article is a stock analysis of NVDIA in the era of AI, why am I even bothering about talking about GPUs and miscommunications?

Because gaming GPUs used to be their main segment, and that the communication on their ability to align to the demand is something that has been concerning and one could think that the market may have overvalued the capacity of NVIDIA to adapt enough to cover the demand for Artificial Intelligence products and potential applications. One could even go further and see it the contrarian way: is there a possibility that the overall sentiment concerning AI technologies might be slightly too optimistic ?

Here are some potential reasons why the demand for AI might not be as massive as it is expected to be:

Hype and Speculation: There could be excessive hype and speculation surrounding AI technologies, leading to inflated expectations of its capabilities and market potential. If this hype is not met with corresponding tangible results or if the technology fails to deliver as expected, it could lead to a correction in valuations.

Uncertain ROI: While AI has immense potential to transform industries and drive innovation, the actual return on investment (ROI) from AI projects may not always meet expectations. If companies invest heavily in AI initiatives without achieving the desired outcomes, it could lead to skepticism about the actual value and sustainability of AI technology.

Market Saturation: As more companies enter the AI market, competition intensifies, leading to saturation in certain segments or oversupply of AI solutions. This could drive down prices and margins, making it challenging for companies to justify high valuations based on AI-related revenues alone.

Regulatory and Ethical Concerns: Concerns about data privacy, algorithmic bias, and regulatory scrutiny could dampen the growth prospects of AI technologies. If regulatory constraints increase or public sentiment shifts against AI due to ethical concerns, it could hinder the adoption and commercialization of AI solutions, impacting their perceived value.

Technology Limitations: Despite significant advancements, AI technologies still have limitations and challenges to overcome, such as robustness, interpretability, and scalability. If these limitations become more apparent or if breakthroughs in AI research fail to materialize as expected, it could temper enthusiasm and valuations in the AI space.

Economic Downturn: Economic downturns or global uncertainties can affect investment priorities and discretionary spending on AI initiatives. If companies prioritize cost-cutting measures over long-term strategic investments during economic downturns, it could slow down the growth of the AI market and lead to reevaluation of its valuation.

For an interesting approach on the subject, I consider that it would be considerably of value to compare the stock market boom related to AI (Artificial Intelligence) to the boom and subsequent crash of the internet bubble in the late 1990s and early 2000s.

As you know, during the late 1990s, there was an extraordinary level of hype and speculation surrounding internet-related stocks. Many companies with little to no profits experienced exponential stock price growth based on the expectation of future profitability.

Similarly, there has been significant hype and speculation surrounding AI technologies, with investors pouring money into companies involved in AI development, regardless of their current profitability or revenue streams. The promise of AI to revolutionize industries has led to high valuations for AI-related stocks, which may mean one thing: to this day, is the market properly valuating NVDIA?

You certainly understand that valuations of internet stocks reached unsustainable levels during the late 1990s, with price-to-earnings ratios soaring to astronomical heights. Many companies were trading at valuations that far exceeded their intrinsic value.

AI Boom: Similarly, valuations of AI-related stocks have reached elevated levels, with some companies trading at high price-to-earnings ratios relative to their earnings potential. Investors are often willing to pay a premium for exposure to the potential growth of AI technologies.

Investor Behavior:

Internet Bubble: During the internet bubble, investors exhibited speculative behavior, chasing high-flying internet stocks based on momentum rather than fundamental analysis. Many investors were focused on short-term gains rather than the long-term viability of the companies they were investing in.

AI Boom: In the current AI boom, there is also a degree of speculative behavior, with investors flocking to AI-related stocks based on the promise of future growth and technological innovation. However, there is also a greater understanding of the underlying technologies driving the AI revolution, leading to more informed investment decisions.

Market Correction:

Internet Bubble: The bursting of the internet bubble led to a significant market correction, with many internet stocks experiencing sharp declines in value. Companies with weak fundamentals and unsustainable business models were particularly hard hit, leading to widespread investor losses.

AI Boom: While there may be concerns about the sustainability of current AI-related valuations, it remains to be seen whether there will be a similar market correction as experienced during the internet bubble. Factors such as continued technological advancements, regulatory developments, and broader market trends will influence the future trajectory of AI-related stocks.

Overall, while there are similarities between the stock market boom related to AI and the internet bubble, there are also significant differences in terms of the underlying technologies, market dynamics, and investor behavior. It’s essential for investors to conduct thorough due diligence and consider the long-term fundamentals of companies when investing in AI-related stocks.

Based on these considerations, it’s possible that even if NVIDIA’s last earnings are very impressive, the market price may not fully capture its intrinsic value due to factors such as overly optimistic expectations, market sentiment, or speculative trading. Therefore, it is our job as investors to conduct a comprehensive analysis beyond just earnings figures to make informed decisions about the stock, and finally decide if the stock is currently overvalued because of wrong assumptions about the future and/or if it is because the stock has become a vehicle for craziness, meaning that it is just a matter of time before the bubble blows up.

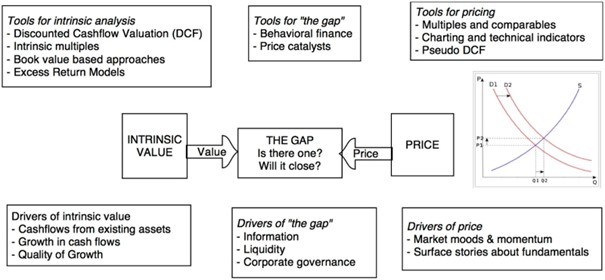

As we understand the distinction between Price and Value, the concept that the stock price could greatly deviate from the true value of the stock is something that, as value investors, we truly dread in the measure that it could be symptomatic of the stock being played around by irrational investors. It means that as good as your valuation is, it could be discarded by the market’s folie of grandeurs, and means that as a value investor, you have no edge against those odds. Therefore, it is of much importance to understand which drivers are moving the stock. The gap, as exposed in Damodaran’s illustration, must be analyzed to decide if that gap might be too important for our taste, and in the case of NVDIA, it is my opinion that the gap is getting bigger and bigger, and that the current price of the stock is mostly driven by momentum and accrued optimism.

Nonetheless, it is still required to value the intrinsic value of the company to prove my point, and add that last point to the multiple reasons allowing me to safely claim how unsound the market has become concerning NVIDIA.

Obviously, this is my model, using my own assumptions so I totally advocate for you to do your own valuation but without any surprises, the stock is overvalued by a lot and does not follow fundamental analysis. I have to mention that this valuation follows optimistic growth rates expectancies and that still does not justify a valuation at 792$ per share.

From what I can tell, the market expects more of an growth rate around the 40% which will slowly degrades around the 4% range in the next decade, taking the optimistic road a little too far in my opinion.

Finally, I want to conclude in stating that while, as value investors, we only play around with what we know, meaning that our approach tries to be as close as reality as we can, and that the only truly analystic tool that we dispose is our fundamental analysis, NVDIA is an interesting case study of valuation being ignored by the market. Meaning that this stock is probably not living under normal rules anymore, and is subjected mainly to speculation, while totally ignoring the fundamental nature of intrinsic value and future cash flows. As Graham said, in the short run the market is a voting machine. Right now, that gap is truly imposing itself as the market has been “saved” by NVIDIA, but in the future the weighing machine will show if the valuation that the market has made about the stock is accurate or not, or if this reality will be ignored. And even if the gap Price vs Value close itself or not, is there a future in which we are going to witness an exceptional example of fundamentals being ignored in the valuation process, pushing the stock to the moon?

At this point, either the market has unrealistic expectations concerning future cash flows, either the stock has become a vehicle for speculation and crazyness. In either case, I’ll never engage in owning stocks that maintain their route in this area of uncertainty. Recognizing that sometimes you don’t have an edge is an important lesson.

The time will tell us if I was right or not on the subject and if an AI bubble has taken place, but my rational perspective on the subject is that NVIDIA’s share price is long due for a correction, but as I said, time will tell.

Everyone that has a TV or does his groceries, knows this simple fact:

Inflation has been back for a few years now, and the purchasing power of everyone has been diminished. Reported numbers such as CPI, PPI and GDP deflators have been strongly highlighting that we have seen higher inflation now that we have seen in a decade and even if your president is saying that we have attained the peak, you still need to comprehend something:

Your savings are never going to be safe if you don’t take matters in your own hands.

It is undetermined at this point if this inflation phase is transitory or permanent, what we know is that in either case, you must be prepared.

To simplify my demonstration, I’m going to use the simplified Keynesian model:

He assumed that: R = C + I where R= revenues, C= consumer spending and I= investments. Which also means that I = R – C.

At this point, you already know that wages can be increased to oppose the inflation, but it is almost never enough to compensate. While consumer spending is also increasing due to rising prices, you can obviously guess that the amount of capital available to invest is going to decrease. In that sense, it is definitely going to complicate your capacity to improve your financial situation.

Furthermore, even if you assumes that the amount of savings that you can monthly put aside is going to stay the same, the simple fact that this amount is tied to your currency means that that you are losing value due to currencies being exposed to different levels of inflation (this is why interest rates vary across currencies over time). Meaning that, for example, if you can monthly save 1000$ in a period of inflation or not, this amount is going to be affected by the fact that your purchasing power has been weakened. 1000$ in a period of inflation and 1000$ in a period of deflation do not have the same value. Therefore, you are losing money, EVEN if you are able to save the same amount.

If you think about it, the saving rate in the euro area was at 14.8% in Q2 2023 which means that the issue of having a capital that is deteriorating due to inflation is not concerning that many people since only a small percentage is able to save money. But for those that actually save money each month, you have to ask yourself: Off that percentage, how many of them actually invest a moderate amount and do not let it just sleep in their bank account?

Even more, do you admit that the common investing vehicle for most individuals is bonds, either by the means of a broker or a legally regulated savings account promoted by your bank which returns at its maximum a yield of 5 to 6%.

Do you think that it is enough to compensate the loss in value of your currency and of your purchasing power? It is common knowledge that inflation is a bond’s worst enemy because for an investor relying on a stream of fixed income payments, higher inflation reduces the purchasing power of fixed payments since those payments stay equal during that period. To be short, payments remain fixed while the price of goods and services increases. If you add the fact that the value of those bonds is depreciating since bonds that reflect better future rate are issued after that Central Banks have raised interest rates, you truly end up at the wrong end of the rope.

To conclude, your long term savings are not going to survive the inflation if you don’t have a proper strategy in place. For those that cannot save up money, themselves cannot be saved. For those that do save up money, but do not do anything with it, they cannot be saved. For those that let their bank counselor invests their savings into bonds or insurances, they cannot be saved.

But the one that can be saved, are the ones that realize that investing should be something that is absolutely and utterly taken seriously as priority to secure your future.

Value investing is an investment strategy which consists simply of purchasing shares whose price is lower than their intrinsic value. The idea is to take advantage of the undervaluation of the market to realize a long-term capital gain.

Sounds easy, right? Damodaran used the term “investing for grown ups” to explain and caricature that type of investing since you need to have a certain maturity to perform that strategy, in opposition to a childish investing strategy which could consist in fast gains appetite and a short temper.

Value investing has a long and rich history, dating back to the 1930s, when Benjamin Graham and David Dodd wrote the classic book, “The Intelligent Investor”. Graham and Dodd advocated for a conservative and disciplined approach to investing, based on rigorous analysis and a margin of safety. They also distinguished between two types of value investors: passive and active. Passive value investors buy a diversified portfolio of cheap stocks and hold them for the long term, while active value investors look for special situations, such as mergers, spin-offs, or restructurings, that can unlock value (see You can be a stock market genius: (even if you’re not too smart) : uncover the secret hiding places of stock market profits from Greenblatt).

Therefore, value investing is based on a few key principles on which I will expand on further below:

Fundamental analysis: this involves studying the financial statements of the company, its profitability, its growth, its competitive situation, its capacity to generate cash flow, its value of assets and every fundamental data at your disposition to be able to determine a correct intrinsic value of the company, which may be different from its stock market value. This search & read process is what is going to allow you to confirm if the company is worth your investment or not, this is how you become familiar with the business and its long term viability, therefore convincing you that you do not need to look at the stock price for the next five years if needed.

Inefficient market theory: Value investing is based on the idea that markets make mistakes, and that some stocks are priced below their true value. Value investors try to exploit these mistakes by buying undervalued stocks and holding them until the market corrects itself.

Source: Damodaran.

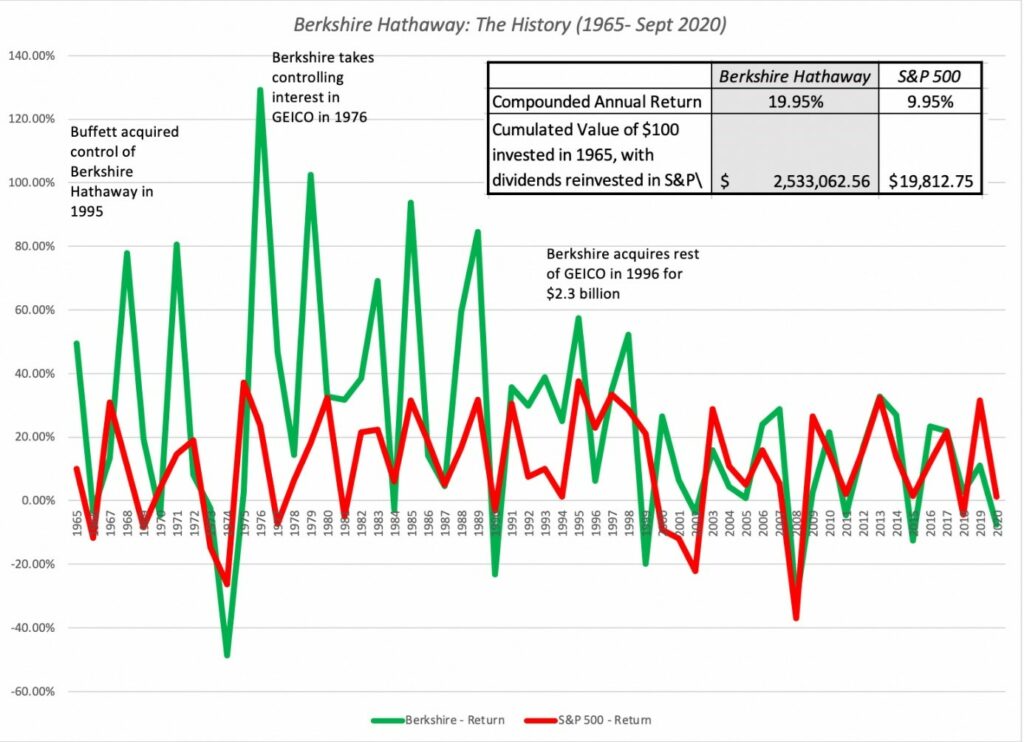

Berkshire Hathaway, Buffett’s company, is a classic example that the market can be inefficient in its ability to properly estimate the value of stocks, and it can be highlighted in this graph: Berkshire Hathaway has been to able to compound an annual return on sixty years which beats the S&P 500 (commonly used index to represent the US Stock Market), proving the point that abnormal returns can be generated using that specific strategy.

The margin of safety: this is the difference between the purchase price and the intrinsic value of the action. The higher the safety margin, the lower the risk of losing money. The value investor seeks to purchase stocks with a sufficient margin of safety to protect against market fluctuations and valuation errors which are unfortunately very common and need to be taken into consideration as part of the value investing strategy.

Time: value investing is a long-term strategy, which requires patience and discipline. Value investors do not allow themselves to be influenced by short-term market fluctuations but focus on the long-term performance of the company. It waits for the market to recognize the true value of the company and for the stock price to adjust accordingly.

While I am certain that value investing is the right way to invest for a logical and calm individual, it is important to mention that stories of value investors and their winning stocks backed up by numbers on how well value investing does, relative to other philosophies, are not sufficient to highlight that you can identify as a value investor and still fail.

That is why, it is of the highest priority to spend enough time studying this school of investing in the hope that you can one day, in the best scenario: challenge compounded annual returns from legendary investors. And in the worst scenario: not become a failed investor and lose parts of your capital.

Calling yourself a value investor, like many things in life, must be deserved through the means of hard work and mistakes well learned.

01/17/2024

To invest or to speculate: to invest or not to invest

A lesson that I’ve learned these last few years and that can be applied to many things, is that there are elements of comprehension I knew innately as they were obvious. But if you take those same elements and present them to a large concentration of people, they would absolutely require you to demonstrate with all of your skills that what you claim is true. And there is a chance that it is not going to being enough.

In regard to investing or speculating, the same rule applies even more accurately and why wouldn’t it be. The nature of investing is deeply tied to feelings of inadequacy and hopes for a better future, therefore it makes sense that sentiments could path their way in the investing process. It should be of value to remind anyone that needs to hear it that decision-making should never lay entirely on the emotional side of our mind. Even more, I would insist on stating that the less emotional a decision is, the better it is. Nonetheless, it is easier than said and we cannot all be psychopaths, feelings are natural and cannot be avoided but it is important to be better and to focus more on what is factual than what the sentiment is. For some of us, it is a natural gift, for some it is something that should be reinstated as part of your investment mindset, so I advise you to figure out what kind of investor you want to be.

Benjamin Graham attempted a precise definition of investing and speculation in his seminal work Security Analysis (1934): “An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

How much you estimate the value of analysis and risk management will dictate the kind of investor you can be, are you longing for certain success that can come in 40 years, or do you want to risk it all to have a very low chance of making it? Most people pick the latter because they do not have the patience and discipline to just aim for a long-term goal, and that is even more true in today’s age since our reward system is completely obliterated. We drudge to pursue goals that are not in hands reach because our dopamine receptors are fried and I only need to remind you that none of your ancestors since the beginning of time has ever felt the amount of dopamine levels that you daily perceive, to convince you.

Another point of view that can be pointed out is the major fact that our generation actually believes that rapid wealth is a possibility because they are polluted by twenty years old crypto-influencers that “made it” or other no-value courses sellers that are currently living in Dubai. No need to expand any longer on why I will not promote this delusional path to wealth, because even if you make it (which is a big if), the path you will have taken to attain that status will have no value that will make you feel good about yourself. If you understand that, you understand that money is not everything and that the path is the reward.

People love to dream, so they love to speculate. To speculate is to lack substantial resources to actually do the job, that is why if you actually believe in the value of work and well-deserved rewards, speculation has no interest for you. Because at your age, you understood that what comes your way can be luck but more often is something that is provoked. I could rant about the value of work and how it has been lost, but this is not the point of this article.

The opposition between investing and speculating is deeply tied to the lens from which you look at the market. Are you in for a short but rattled time, or are you in for a slow and boring win.

This short time can be good or bad, to be able to grasp if returns on speculative trading is profitable you shall ask yourself if it is backed by anything substantial besides technical analysis, news and sentiments. If looking at a triangle pattern or a last-minute news stating that X stock is going to drop because sales are going down in the next quarter, I want to ask you:

Do you really think that there are not algorithms doing that job better than a human speculator would? The fact is that long term, only a small amount of options trader will perform well, and you are probably not going to be that person, and this is okay.

I like to see the market as Benjamin Graham did: Mr. Market is an allegory to describe that the market is full of irrational and contradictory behaviors. Do you want to try to follow each swing of Mr. Market, hoping to catch the trend, without any factual tools to achieve that goal? Or do you want to ignore Mr. Market, and realize that looking at it from a short term perspective is that the Market follows mostly manic-depressive behaviors, but that from long term perspective it is the actual value of the stock that has the last say.

As Graham said, the stock market is a voting machine in the short run but a weighing machine in the long run. Therefore, value and truth will always prevail and I like to see things that way.

I personally find that fundamental investing, laying on rationality, has no need to convince me to understand that it just makes sense. It makes sense to analyze, it makes sense to be convinced by the well searched value of a stock to know that this investment does not require from you to spend each minute of your life looking at Bloomberg terminal to see if the share price dropped or not. I like to live a calm life so I am encouraged to separate myself from irrational entities and so should you.

Individuals such as Guy Spier or Mohnish Pabrai, to only cite them, when first read about value investing , were just automatically convinced that it was for them, and that it was their way to win. And I totally bear witness to that truth.

The concept that you should look at owning a stock as owning a portion of a business is not something that a speculator would even care about. But for someone looking to be in it for the long game, it is of essence, thanks to Buffett and Munger, that owning stocks of great companies is the solution. You don’t want to own a share of a company in which you don’t believe in, even if you are going to make a buck out of it. If you are in it for the long haul, you should try to hold long term. Would you be confident in being the owner of a dying business, even if you can make sell at a gain? Buying cigars butts (companies that still have one last puff in them) is good, but not great, and you don’t want to look at the whole process as being a vulture, eating on the dead.

You want to be there to build, to increase the value, because the fundamental point of shareholding is that: you lend capital to a company, in exchange for a share. The company is going to use that capital to grow, and going to reward you with the Free Cash Flow that it was able to produce thanks to your interest in the business. That process is healthy and was the original purpose behind shareholding. I would even go further and say that investing should only go in that directing, reinstating the difference between investing and trading. As an investor, you are exchanging capital to grow something, it can be a business, a venture or even a building. You invest because you want to increase the value and sell at a positive return. In stock trading, you may not have to sell and can possibly own a stock till the day you die. But in comparison, what does the speculator gain from that process, is he there to build? Is he there to produce value? For these reasons, we can only admit that investing will always be a much nourishing and healthier process than speculating.

True value is built over time, and yes you can certainly partake in the stock market in many ways and speculate, short and put options and just have fun. But if you are truly looking to be an investor, you should understand what an investor is and align your thought process with all the elements composing the intrinsic nature of investing.

You can gain a lot from simplifying concepts, in contradiction to details analysis and connections processes. In mathematics and logic, demonstration requires that a collective number of structured steps must be taken to attain the goal of finding proof. That is the type of reasoning I used in this article: starting from a definition of what is the essence of investing and only going from there, and then moving forward into details and micro vision, to finally highlight how coherent and vibrant fundamental investing is, and obviously dismiss the speculative mindset.

To be even simpler, it makes sense to create value in your portfolio (increasing your returns), and therefore in your life (by enjoying the intellectual process), if you just concentrate your attention on the value creation process, in opposition to a speculative strategy that absolutely discard this variable. I used to be a fervent admirer of complicating things but sometimes you just need to admit that by focusing on simple reasoning as a starting point and as a macro vision overview, you reduce your probability of invalid proof.

However, I would like to start by saying that if you read these words with the umpteenth conviction that this is yet another guy who wants to sell you his ultimate method or who is lying to you about how he is going to do it: you are deceived. I’m not going to be like all these guys who are trying to sell you courses to get rich, while they become rich thanks to the fact that they sell courses. Indeed, I am not here to sell you anything, but simply to make you a witness of my journey and the completion of my goal: to become a millionaire.

Perhaps it is necessary that I tell you a little about myself, you must tell yourself who is this arrogant man, who believes that he can become a millionaire just because he decides to do so. I am you, I am me, I am someone who starts from zero. No inherited wealth, nothing, nada. Just an ambition, a finance degree obtained with excellent results, and a sufficiently intelligent brain, no more, no less. I think relatively few people these days really believe in the possibility of achieving a moderate level of wealth and for these people I would like to tell you that it is rather not to become rich if you spend less than you earn and invest regularly through the power of compounding interest. I understand that the goal itself of “becoming a millionaire” probably seems unattainable for many, but I have a plan, or at least a financial strategy. I have been studying the school of thought invented by Benjamin Graham for some time now, which is called “value investing”. And today I can say with conviction that becoming a millionaire by being regular, patient and above all rational does not seem impossible to me. I would even go so far as to say that unlike getting rich quick and seeing yourself fail 99.9%, getting rich slowly but surely seems to me to be a much more logical approach, but who has the patience to do that these days?

Thanks to the knowledge of my spiritual mentors like Warren Buffett, Joel Greenblatt, Mohnish Pabrai and Guy Spier, to name a few, I intend to achieve what they accomplished before me by relying on their experiences. Obviously, we are not at the same time and I am just an ordinary individual, but I believe in the power of rationality in the face of emotional players in the stock market. I started less than a year ago with zero capital, and today have a portfolio worth around €12k. This is only the first step towards my goal, since I am already at 1% out of 100 by just investing my savings monthly, and through the power of cumulative interest I envisage in the worst case scenario being a millionaire by 18 years old. I will use all means at my disposal to achieve this objective as quickly as possible, without disregarding the risks I could take. Rationality above all. It therefore appears that my objective is indeed to fill my pockets, but it is only an externality to an intellectual investment process that fascinates me. I’m not doing all this to be a millionaire, I’m doing this because I’m passionate about it. Having my own investment fund that would allow me to practice and make a living from my passion is something that drives me and this blog will therefore serve as my journal. Ambition is not pretension, I believe that we must give ourselves the means to accomplish what we dream of, I believe in my abilities, I continue to learn and every day that God brings me closer to my goal little by little.

May this statement serve as proof that blindly believing in one’s abilities has a power that no one can deny.